Martin Wittmann is ams Osram’s Senior Director of Global Marketing for the Opto Semiconductors Visualization & Sensing business line. Since 2016 at Osram, he has held positions including Manager and Head of Global Marketing for the Sensing Division.

He holds a diploma in electrical engineering (microelectronics) form the University of Applied Sciences in Regensburg. He graciously shared his thoughts with us:

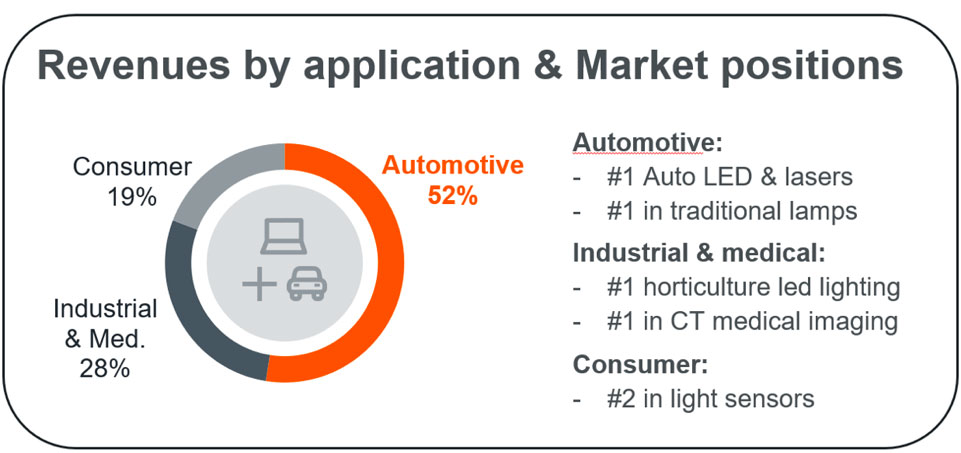

DVN: ams Osram develops optoelectronic components for mobile, medical, and automotive applications. What is your global turnover and the share of the automobile segment?

Martin Wittmann: ams Osram had a revenue of €3.59bn in 2023, with a split of around 50 per cent for the automotive market which is very important to us. Especially for Opto Semiconductors segment (OS), revenues increased by €9m to €381m in Q3-24 compared to €372m in Q2-24. Details are in the shareholder reports.

DVN: Could you tell us more about your portfolio and the automotive applications you target?

M.W.: ams Osram’s portfolio for automotive applications addresses megatrends such as energy efficiency & sustainability and digitalization with projected lighting, smart surfaces, and advanced displays. Our portfolio contains prize-awarded dynamic forward & signal lighting, in-cabin sensing, and ADAS/AD sensing which leads me to lidar.

DVN: For ADAS / AD sensing systems, ams Osram has great experience with laser sources for lidars. What are the main components and the new technologies and components coming in the near future?

M.W.: ams Osram lidar offers a wide range of laser components such as bare die lasers, plastic radial packages, TO cans, as well as automotive-qualified SMT packages. They range between 25 and 1000 W and suit automotive and industry customers.

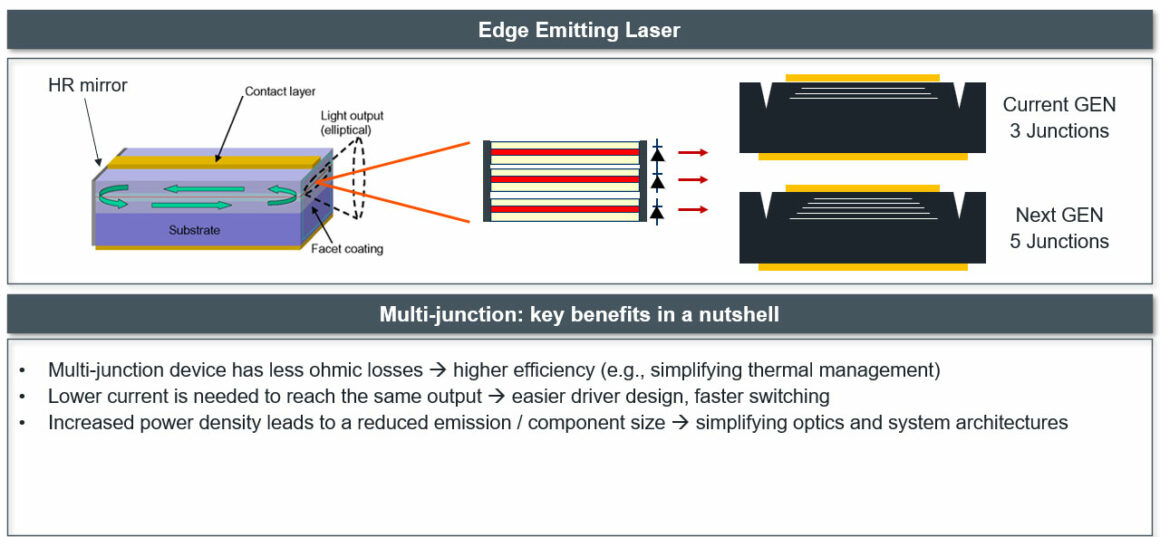

Our latest product, presented at the DVN conference in Wiesbaden, is a 5-junction edge emitting laser chip (EEL). By implementing our new 5-junction technology with our wavelength stabilization, we can reduce the heat dissipation for some operation conditions by over a factor of 2. Alternatively, 5-junction technology can double the optical peak power output of a single channel EEL.

DVN: How do you see the cost curve for lidar Sensors? Can we expect breakthroughs?

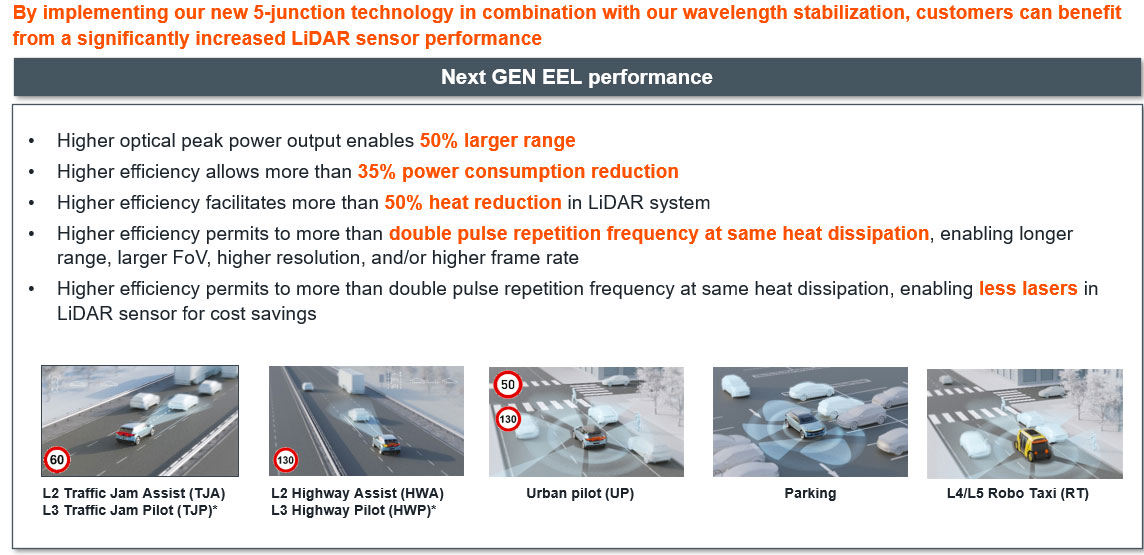

M.W.: Similar to what we experienced in the past for other emerging automotive applications, we expect that the Sensor ASPs will become more attractive thanks to the strong efforts on BOM optimization and increasing economy of scale. For the semiconductor portion of the BOM which includes our laser diodes, high volume is key to further reduce cost and our team is constantly working on increasing the laser performance to enable new lidar sensor designs. One key breakthrough is of course our new 5-junction laser diode. Its higher efficiency permits more than double the pulse repetition frequency at the same heat dissipation, which gives lidar manufacturers more room to optimized sensor performance and cost.

DVN: Do you see new applications like short-range lidar emerging soon? Do they need specific components?

M.W.: We see short-range lidar for L4 trucking emerging soon. Also, the Robotaxi market is expanding as well as players in the Chinese Market who have permits to explore L4 driving in China. All of them have short-range lidar included. There are no standard solutions established so far, and EEL and VCSEL as well as various scanning solutions are emerging.

DVN: What is your opinion on FMCW?

M.W.: ams Osram is currently observing the progress of FMCW as the current market share is limited according to industry reports like Yole. Technical hurdles are to be solved before implementing the technology in passenger cars with large field of view, high resolution and low power consumption as required by most OEMs.

DVN: For AD L3 and L4 sensing systems, there is a debate between Camera + Radar + lidar (most makers) and just Cameras + ‘AI’ (Tesla). What is your opinion about the two different strategies?

M.W.: Camera technology in ADAS systems is a well developed technology with the most miles driven. Considering, though, the limitations that cameras have in all other-than-perfect conditions, we see full redundancy including lidar as mandatory, especially for L3 and L4 sensing systems.

Especially in safety-critical applications, we believe lidar is a must which is also the consensus amongst the majority of OEMs.